RSS Feed

RSS Feed

Bonds Bonanza 2: Bonds Go Banana

06 Jun 2021in Finance

In the last post I explained the basics of the bonds market, the difference the interest rate and the yield, etc.

I also mentioned that in February, yields soared from 1.13% to 1.6%, causing a large upset in the stock market as well. In this post, I want to look at why this happens, and how the effect spilled over to the stock market.

Be warned that this post is a bit more about figuring things out than presenting orderly facts. I'm far from mastering all the variables here, so take everything with a grain of salt.

The Fundamentals

The basic explanation of why the bond prices dropped precipitously and the yield soared is pretty simple: people expect US dollar inflation, meaning rising prices, hence a currency with less purchasing power. Inflation does all kinds of bad things to the economy (which we will examine shortly) and so the federal reserve tries to keep it subdued. It does this mostly by increasing the interest rates it pays on newly emitted bonds. This decreases bond prices and increases bond yield.

If it's not clear to you why the federal reserve increasing the interest rate on bonds leads to falling bonds price and thus higher yields, see the previous article.

Remember that government bonds are the ultimate safe investment. Raising the interest rate leads to a bunch of other interest rates in the economy to increase (for instance, on savings accounts), which promotes savings, which reduces the amount of money circulating in the economy. The federal reserve also uses the federal funds rate to achieve this objective. (Sorry if this is not very precise. I wish I had a better understanding of the mechanics here.)

Reducing the amount of money circulating is important, because inflation is caused by a changing balance between demand and supply. When there is a lot of money chasing few goods, prices increase, and you have inflation. You reduce inflation by decreasing the amount of money in circulation, or by increasing the amount of good produced.

People expect inflation, of course, because Joe Biden signed a stimulus bill where the government would spend 1.9T$ (that's trillion). For reference, the total market capitalization (summing the value of every share) of the S&P 500 is about 30T$. Then there is a 2T$ infrastructure bill being debated right now, and there might some more down the line. When you inject so much money in the economy, inflation is not exactly unexpected. There is however much debate about how high inflation will go, and how transitory or persistent the increase will be. The federal reserve currently maintains that the inflation rate might rise over 2%, but that this should only be temporary.

The only uncertainty in all of this is if, or whether when, the federal reserve would increase the interest rate in response to inflation increasing. The price move caused such an uproar because the federal reserved had been saying (and has kept saying since) that they don't expect to increase the rate anytime soon and that it's fine if "the economy runs hot" and inflation is temporarily increased. The bond market seemed to be saying that either the situation would be worse than the fed expected, forcing its hand, or that, under pressure from the markets, it couldn't walk the line (as seen in the 2013 "taper tantrum").

Once the move was initiated, however, it made sense for most people to follow suit. Whether you're a trader or a long-term investor in long-term bonds, you expect the rates to increase eventually, meaning it will be profitable for you to sell your bonds and buy new higher-rate bonds. If the bond price starts to drop, you should therefore sell. In fact, the only reasons not to sell are if either you don't believe the rates will increase or if you're contractually obligated to hold bonds instead of cash.

But on top of this strong fundamental reason, there were a few other catalysts and technical details that can help explain the sudden move.

A first catalyst (source):

Back in April, the Federal Reserve tweaked its rules to exempt Treasuries from banks’ supplementary leverage ratios — allowing them to expand their balance sheets with U.S. debt. But that relief ends March 31 and what happens next is something of a mystery.

So it was expected that by April 2021, banks would have offloaded excess bonds to get back in cash and satisfy the re-tightened rules.

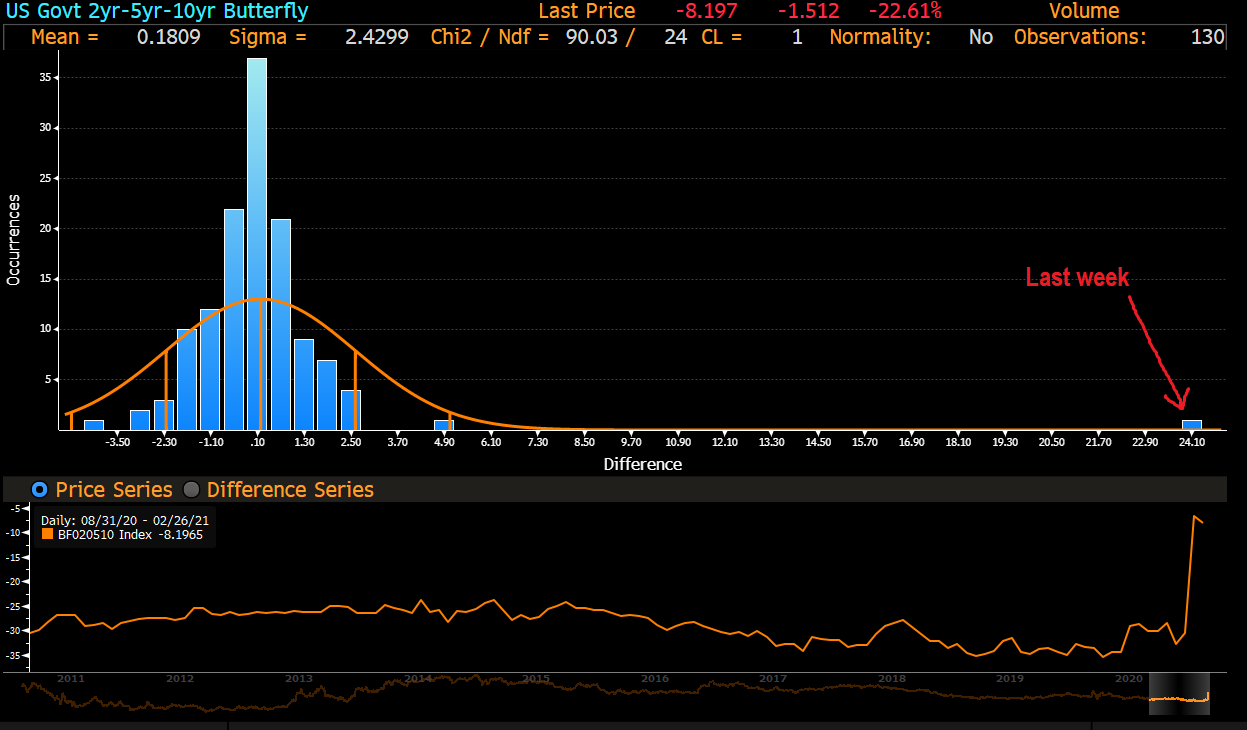

Bonds Butterfly

With all these bearish expectations towards bonds, the market just needed something to light the fuse. The catalyst was probably an auction of 7-year bonds seeing record low demand. Remember from last time that bonds are initially auctioned by the fed, so low demand would have caused these bonds have a low price and a high yield. This in turn caused the associated but more common 5-year bonds to drop a whopping 0.75%.

This made a lot of people happy, as the 2-5-10 butterfly is a popular trade:

The butterfly strategy involves buying both long and short-term bonds while simultaneously selling medium-term bonds. This strategy is designed to help investors profit from predicted fluctuations to the yield curve.

... The purchase and sales cancel each other out, making this a theoretically zero-cost investment. This has the impact of cancelling out any shifts in the overall values of the bonds unless the shifts are disproportionately weighted to one maturity over another. When disproportionate shifts occur, the investor can earn a net return. ...

One common butterfly trade involves three treasury bonds. The investor sells five-year treasuries and buys two- and ten-year bonds with the money that he receives in a proportion that makes the average life of the portfolio equal to five years. To do this, the portfolio would be slightly more heavily weighted towards the two-year bond. To begin with, the idea is for the blended yield of the two- and ten-year bonds to be higher than the five-year bond's yield. The other advantage of the butterfly is that if the relationship in yields changes, it could increase returns.

It must be noted how remarkable these events are:

Tracy Alloway notes that, “The 2/5/10-year butterfly — a popular trade involving two-, five- and 10-year U.S. bonds — moved by an astonishing 24 basis points (one of those events which, when measured by standard deviations, is only supposed to happen once in a billion years, etc.).”

What I assume happened next is that traders unwound their positions to capitalize on this sudden dip in the 5-years price. Since they were long 10-years bonds, that caused that price to also dip suddenly.

It's hard — if not impossible — to tell, but this might have been the initial shock that set the yield surge in motion.

Shorting

Another straightforward force multiplier to the move was short selling. I talked about short selling in my article on Gamestop, but basically bond short-sellers borrow bonds, sell them, wait for the price to drop to buy them back and return them to the original owner, pocketing the difference as profit.

There was ample evidence of short selling in the bonds market. In particular, the repo market rate for the 10-years bond went to -4% at some point... The what now?

The repo or "repurchase agreement" market is where one party sells a security to another, and agrees to repurchase it later at a higher price. Essentially, it's a collateralized loan.

The repo market allows financial institutions that own lots of securities (e.g. banks, broker-dealers, hedge funds) to borrow cheaply and allows parties with lots of spare cash (e.g. money market mutual funds) to earn a small return on that cash without much risk, because securities, often U.S. Treasury securities, serve as collateral.

The repo market allows financial institutions that own lots of securities (e.g. banks, broker-dealers, hedge funds) to borrow cheaply and allows parties with lots of spare cash (e.g. money market mutual funds) to earn a small return on that cash without much risk, because securities, often U.S. Treasury securities, serve as collateral. (source)

The repo rate typically trades in line with the Federal Reserve’s benchmark federal funds rate at which banks lend reserves to each other overnight.

The fact it went to -4% means that people were willing to pay up to 4% interest for the privilege to borrow 10 years bonds, with the intention to short them and turn a profit. In that market, 4% is a lot, meaning there was a lot of competitive pressure, hence a lot of short selling.

But wait! That's not all. We have another villain in our story in the form of convexity hedging.

Duration, Convexity & Convexity Hedging

Some funds invest in mortgage-backed securities (MBS). Yes, those that caused the great financial crisis and gave us the delightful movie The Big Short — check this excerpt if you want Ryan Gosling to explain bad mortgage-backed securities to you. What a time to be alive.

Anyway, when interest rates decrease, homeowners can refinance their mortgages to lock in a lower rate. This involves paying off part of the remaining loan immediately (hence it is called prepaying). This shortens the mortgages, and as a result the average length of mortgages in the MBS decreases. This causes the duration — the weighted average of the times until when cash flows (loan repayments) are received — to go down. The opposite is also true: when interest rates increase, people don't refinance, and so the average length of mortgages goes up.

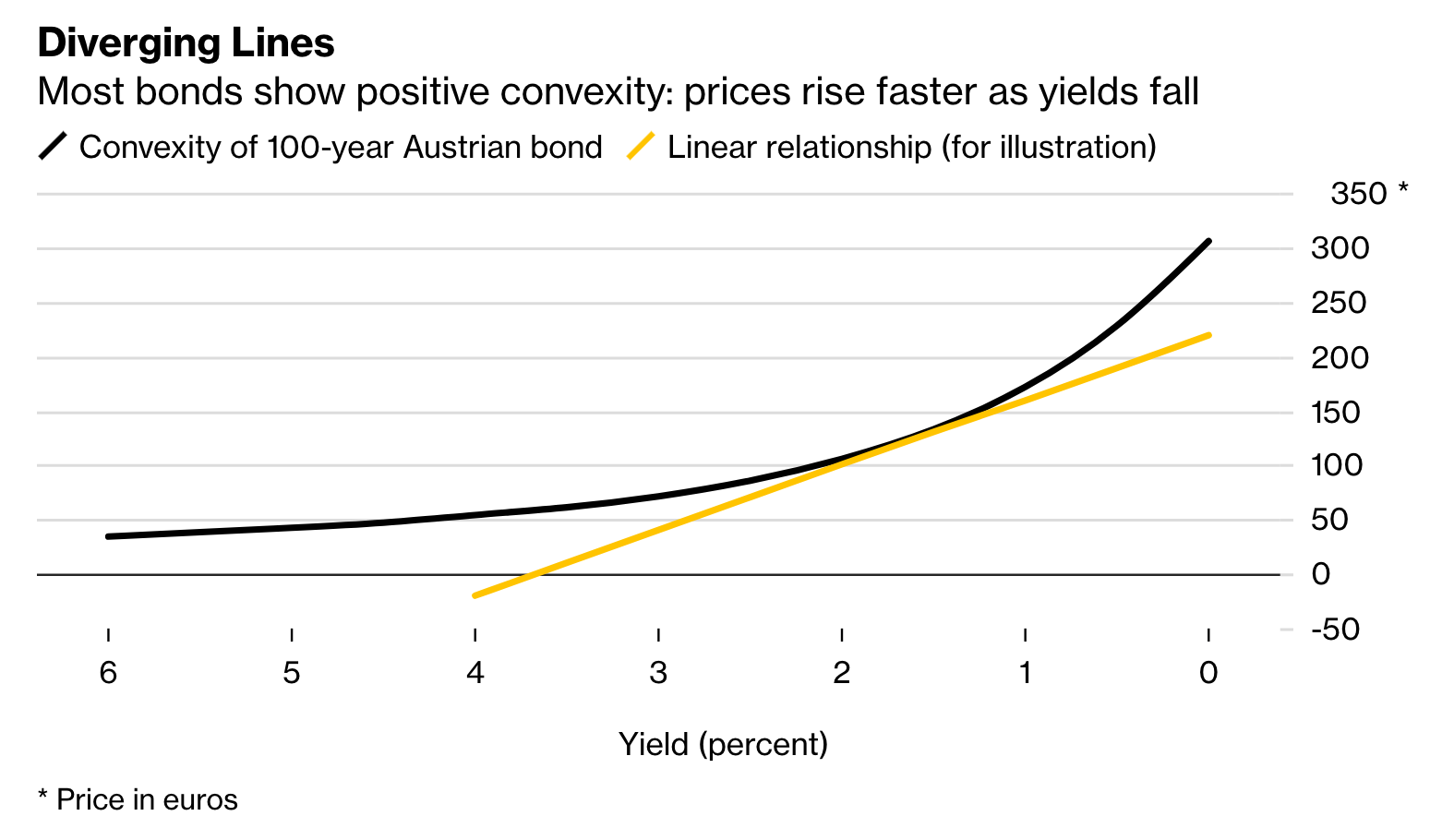

To explain how that impacts the bond market, we need to lay some groundwork. Bonds have a property called convexity — when the interest rate decreases, the price increases more than proportionally, and vice-versa.

Reminder: It's always been unintuitive to me that bond price should rise when interest fall (shouldn't it be the opposite?). So let's tackle that first, then we can tackle the question of proportionality.

To key is that the rate increase will only affect newly emitted bonds. The yield must be constant across all bonds with the same maturity (otherwise it's an arbitrage opportunity). Adding new bonds with lower interest rates tends to push the yield down, hence the price of existing bonds up!

It's not obvious that it would push the yield down. After all, a lackluster auction could bid the new bonds up just enough so that the existing yield doesn't move. It doesn't seem to work like that in practice, and I suspect it's due to the new bonds shifting the expected future yield. As older, higher-interest, bonds expire and newer, lower-interest, bonds are introduced, it does make sense to expect the average yield to go down — at least when ignoring fluctuations in the bond market, and excluding the possibility of a sudden paradigm shift in bond valuation.

So decreasing rates push bond price up. Why do they increase more than proportionally to the decrease in rates? In one word: compounding — when the yield moves, the price move must capture not only the change in coupon payments but the proceeds of reinvesting these payments. For this reason, longer-term bonds are more convex: more interest is being paid. At this point, I'm ready to launch in a long, fascinating (uhm) mathematical digression on yields, duration, compounding and [present value calculations], but this isn't really the point of this piece. Maybe another time?

So bonds have convexity. Mortgage-backed securities, on the other hand, have negative convexity (not sure why they didn't call this "concavity", but whatever). This means that as the interest rates fall, the price increase less than proportionally, or even fall!

First, why would the prices go up? Same reason that the bond yields go up (see above). Since government bonds are the ultimate risk-free security, most other rates in the market depend on them, and will be higher. The difference between the yield for a financial product and the risk-free rate (the bond yield) is called the risk premium. So if bond yields go up, MBS yields are expected to follow suit (at least if we assume that the reason that the yields went up has no material impact on the mortgage market and the default rate).

The reason MBS prices go up less than proportionally (and in any case, less than bond prices) is that, as we said at the start of this section, decreased rates increase mortgage refinancing, which decreases MBS duration — the weighted (by monetary amount) average time of received cashflows (loan repayments). More refinancing and prepaying means less interest payments, though we will recover a larger part of the principal earlier. What the MBS did offer us however was a certain yield (based on the mortgage rate). When the duration decrease, we lose on that yield, and must reinvest the prepaid sums elsewhere — right after the interest rates went down! This loss in compound interest is what causes MBS prices to rise less than expected.

So, bonds have convexity, mortgage-backed securities have negative convexity. What is convexity hedging? It has to do with the facts that the funds that own these MBS include things like pension funds, which have regular cash outflows (e.g. to pay said pensions). This means the cashflows need to be regular. But MBS cashflows vary with interest rates!

To take care of that unpredictability, these funds hedge for duration. Here's how they do it: When interest rates increase, MBS duration increases, and funds sell long-term bonds to cover liquidity needs; when rates decrease, MBS duration decreases, and funds reinvest prepayments into long-term bonds.

Back to our initial topic, the net effect is that when interest rates increase, MBS duration increases, which leads to funds selling off bonds to hedge duration. The opposite happens when interest rates decrease. This naturally amplifies the movement of bonds in either direction (as the bond price is already on the upswing when interest rates decrease).

And with that, we completed our tour of the plausible reasons for the February bond yield surge! Now we need to briefly examinate how this impacted the stock market.

Inflation Redux

Inflation means that money loses value. With inflation, a dollar in a year is worth less than a dollar today. In an ideal world of spherical cows, all prices and wages would update instantly to reflect this new value of money.

If inflation worked like that, it would cause very little trouble. Sure, if you're holding cash, you're suddenly poorer in terms of purchasing power. Conversely, if you're holding debt, you're suddenly "richer" because your repayments are worth less — and your revenues increased proportionally to inflation anyway.

Alas, prices do not update instantly, and it's precisely this transition process that is painful. Inflation works in wave. The first goods whose price increase are those whose price is very liquid. The best example is commodities: ores, oil, grains, etc. In fact, the flare up in lumber price has been in the news quite a bit recently. It's probably unrelated to inflation, but it shows how fast these prices can move.

Commodities are the very beginning of the supply chains involved in the production of most goods. This means that, in the presence of inflation, the increase in price slowly cascades through the supply chain. The increase in price is not reflected immediately for two big reasons: existing commitments and competition. If you already signed a contract to supply a good at a certain price, you're stuck. If you're in a very dynamic market and you can change your price, you might still not want to do so, because your competitors might not have done so yet, and you'll lose customers to them. Of course, they'll have to raise prices too eventually, but these effects slow down the price cascade — it's a coordination problem. Where commodities are concerned, there's also uncertainty as though whether a price increase is just a spike (possibly fueled by speculation (*1)), or a more permanent shift.

At the end of the supply chain lies the final customer, the individual. Unfortunately, wages are typically the last thing to increase in the inflation process. This is because the price increase takes quite some time to reach final consumers, and because the profits of a company must increase (after it can reflect inflation in the price it charges) before it starts paying employees more. And companies will tend to increase pay, if only to get a competitive advantage by poaching promising talent.

(*1) This kind of speculation has, of course, unpleasant side-effects, such as making lumber more expensive for those that have a genuine use for it. However, I want to emphasize that this is the cost you pay for having an efficient market, and an efficient market does buy you something. In particular, it greatly reduces the time for inflation to cascade through the system, and hence the economic pain that results from it. This is what the next section is all about.

What inflation does to companies

So inflation is a painful transition towards higher prices caused by a loss of value of the currency. Inflation occurs when the balance of money and goods shifts in the direction of there being more money and/or less goods. In the current situation, there is more money in circulation due to stimulus and massive public spending (*2), and a modest deficit for goods whose supply chains were shut down during the Covid pandemic.

(*2) At least in the United States, though it seems likely that other parts of the world will suffer from, at least, a milder version of the same problem.

The consequence of this on companies is that they will go through a transition period where their expenses will increase, but their revenues do not increase in kind.

What, then, does inflation do to the valuation of companies? We mentioned two things already. First, there is an impact on the balance sheet: cash loses value, but so do debts. Second, there is a loss of profit due to price lag. In some cases, those are straightforward to compute. In some cases not so much. On top of this, there is the concern that this will put too much strain on the company's finance, which will have to borrow at unattractive rates or, in the worst case, be forced to liquidate.

So inflation is bad for everyone; but depending on balance sheet composition, position within the supply chain and general financial health, it is worse for some companies than for other. But wait — hasn't the S&P 500 has been making consistent all-time highs since the events of February?!

Clearly, to understand why growth stock got hammered in February, we need to look beyond just the fundamental prices in the growth, and into the theory of stock valuation.

Equity Risk Premiums and Hurdle Rate

Pricing the stock of a company is more art than science (otherwise they wouldn't constantly be swinging around even when absolutely nothing of substance happens). Nevertheless, many theoretical frameworks have been proposed to try to explain the factors that underly stock prices, and to try to estimate what a "reasonable" stock price may be.

This is quite the rabbit hole, and if you're interested, the best place to start is Aswath Damodaran's valuation course.

Two concepts that are particularly useful in analyzing the price of stocks are the notion of equity risk premium and that of hurdle rate.

The equity risk premium is the (expected or actual) return on equities in excess to that of the risk-free alternatives. Typically, treasury bonds are used as the risk-free alternatives, the 10-year rate being the most commonly used. So if 10-year bonds have a 2% yield, and the stock market (for instance, the S&P 500 index) returned 12%, then the equity risk premium was 10%. Typically, the equity risk premium is calculated on historical data; there is obviously no guarantee going into the future.

That's the equity risk premium, but the concept of risk premium generalizes to other financial asset and even to sub-classes of stock. Of particular interest to us here is the risk premium for growth stocks and the risk premium for value stocks.

Recall that value stocks are stocks who trade in line with a valuation obtained through some kind of fundamental analysis process. The most common of which is to use discounted flash flows (DCF): computing the present value of the expected net profits of the company for some future period (typically 10 to 20 years). This approach is of course only applicable to profitable companies.

Growth stocks, on the other hand, are companies whose revenues are growing a lot (or are deemed to be poised to grow a lot), but who may not yet be profitable. The valuation is based on future expectations of growth — which may not come to pass and can sometimes be a bit too optimistic.

As the name implies, risk premiums are rewards for risk. Growth stocks are riskier than value stocks, and so should command a higher risk premium. But what is this "risk" we talk about? Consider that a risk premium is an average computed on a basket of stock (or on an index) over a certain period of time. Risk can be seen as the variance between the stocks in the basket, and the variance over time. Growth stocks, for instance, are particularly risky: most innovative companies end up failing, but those who survive tend to have extraordinary growth.

The second important concept is the hurdle rate, which is simply the expected return you demand to take on some amount of risk. Everybody will have its own hurdle rates for different level of risks, though it tends to depend on possible alternative uses of capital and risk-free rates of returns. Just like the risk premium, the hurdle rate increases with perceived risk.

Putting the two concerns together is straightforward. Given a class of assets (e.g. growth stocks) and their associated risks, you come up with a hurdle rate (the return required to convince you to invest in the asset) and a risk premium (the return you expect to earn on top of the risk-free rate). If the total expected return for the asset (risk-free rate + risk premium) is higher than the hurdle rate, you invest, otherwise you don't.

If you want a deeper and more data-driven take on inflation and stock valuation, I recommend this article by Aswath Damodaran. I don't pretend to understand all of it, but it makes very interesting points.

So what happened to growth stocks?

It would be a stretch to say that, as bond yields rose, investors recomputed their hurdle rate up (because the risk-free rate was up) and their expected risk premium down (because inflation was likely, cutting into profits).

But on the other hand... Everyone knew that valuations in the growth segment were historically high on any metric that you cared to consider. This meant the category was particularly risky. Inflation comes in and maybe the risk is now too high given the potential rewards. Better to lock in some profit. This is essentially the hurdle/premium process, but perceived intuitively.

At this point, we also have to mention that inflation might be particularly bad for the typically non-profitable growth companies, as it impedes their ability to raise money. Not only does inflation expectation increase the interest rate on debt, but it means that the money you borrow has lost value by the time you spend it. Inflation also negatively affects the ability to raise cash via stock sales: reflectively from the above, we expect inflation to negatively impact the stock price, which mean that less money will be generated by selling (so you need to sell more of it, which negatively impacts the stock price, ...).

As always whenever we talk markets, we have to consider force multipliers and momentum. As growth stocks sold off in February, it became clear this that this was not a mere fluctuation but a full-blown correction. This causes stockholders that had not reacted to the bond market to start selling too, in reaction to the price movement, but for the same reasons: the upside of continuing to hold longer is limited compared to the immediate risk embedded in the downward trend.

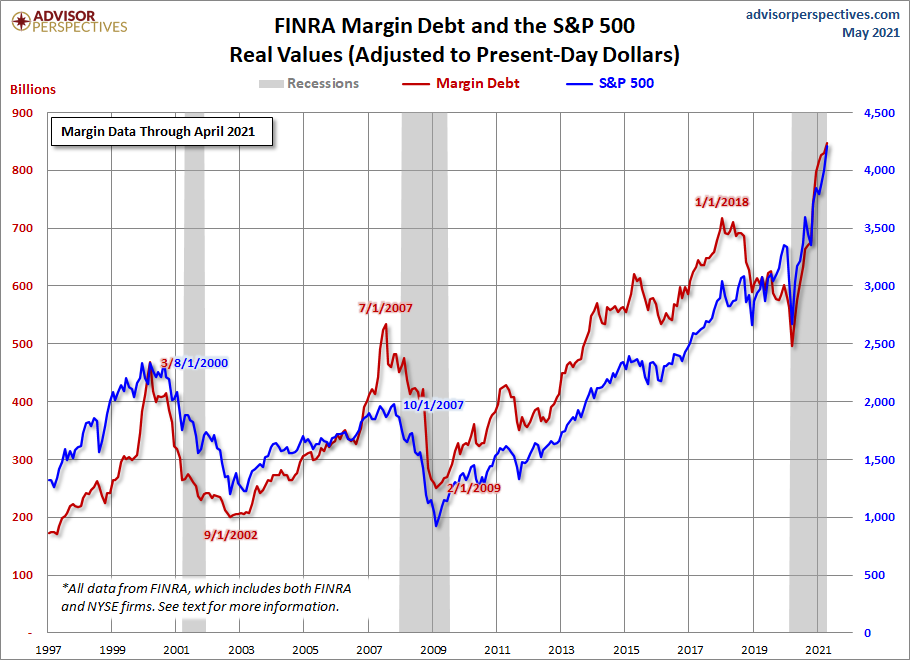

Big moves in the stock market are also driven by de-leveraging: if you purchased stock on margin, a sudden price drop forces you to sell stock to maintain your margin requirements and avoid margin calls. This is especially relevant since margin debt levels are historically high.

The margin debt level may be in line with the S&P 500 price, but note that you would expect the debt ratio to decrease as stock prices go up. If you buy 5k$ worth of stock at 5:1 leverage (so fronting 1k$ of your own cash, taking a 4k$ margin debt), and the stock goes up 20%, your stock is now worth 6k$ and your leverage ratio is now 3:1 (stock worth 6k$, of which 2k$ is not debt). One possible interpretation of the chart is that as stock prices go up investors reinvesting the profits with leverage (i.e. they maintain a constant leverage ratio). Note that the chart also does not say where the leverage is deployed (across the stock market? or is it concentrated in certain stocks?). In the end, it seems that leverage will accentuate any "natural" price move, both in the up and down directions.

Conclusion

So, what happened? What have we learned?

Bond prices decreases and the yield rose, driven by inflation expectations. A series of events catalyzed (the 7-year bond auction) and amplified (the butterfly trade, convexity hedging) this change.

The effect spilled over to the stock market, where it was mostly driven by sentiment, reflecting both the increased risk-free rate and the lowered return expectations due to inflation. Because growth stocks' valuations were stretched, that was all it took to tip this segment of the market into a correction.

When these events transpired, I did not get how inflation and the bond market could influence stock valuation to this extent. In fact, some of my intuitions were to the opposite. For instance, since companies will keep making money in the future, shouldn't inflation push the stock price up to reflect the future revenue increase due to higher prices?

I was also looking for a technical explanation (based on some mechanics of the financial markets), whereas the move seems to have mostly been driven by sentiment and risk-reward considerations. This happened on the heels of the Gamestop gamma squeeze, which had a straightforward technical explanation, so there might be some availability bias there.

If you enjoyed this article, you might enjoy other articles about finance.